Opinion: MJ Estate v. IRS – The already reduced tax amount

Back in 2014 I did a series of opinion pieces on the MJ Estate v. IRS Estate tax dispute. (Link here, here and here).Initially I planned to do more posts getting more technical about tax issues and valuation. However after seeing the confusion even about market value vs. tax value, I realized how complex and boring the tax discussion was for many people. So I scratched my idea of posting more opinion pieces.

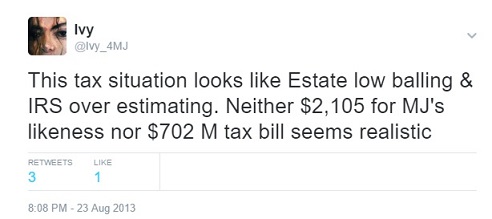

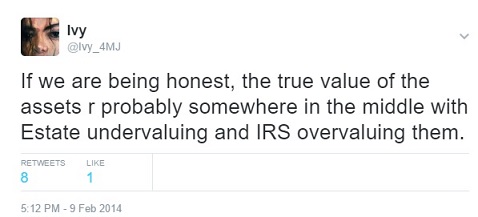

From the start I believed that the true tax amount was in the middle of what MJ Estate and IRS were saying. A further look into other similar disputes confirmed this belief. So I did not see any real benefit in speculating and even arguing about what the final tax amount would be. Plus I thought the parties would come to a settlement rather quickly. Unfortunately I was wrong.

|

|

By the time the trial finally started in February 2017, I was focused on other cases. I still felt the same way about IRS case – that I did not want to do technical complex (and even boring) posts and that the true amount was somewhere in the middle. I was optimistic that a major media source would report on the case regularly but that did not happen. While media occasionally reported intriguing testimony, they too did not seem to be interested in reporting the complex valuation issues.

However one thing from the opening statements stood out to me. It seemed like neither the media nor the majority of the fans were realizing that the tax deficiency had already been significantly reduced.